By making a personal super contribution and claiming the amount as a tax deduction, you may be able to pay less tax and invest more in super.

How does the strategy work?

If you make a personal super contribution, you may be able to claim the contribution as a tax deduction and reduce your taxable income. The contribution will generally be taxed in the fund at the concessional rate of up to 15%1, instead of your marginal tax rate which could be up to 47%2. Depending on your circumstances, this strategy could result in a tax saving of up to 32% and enable you to increase your super3.

How do you claim the deduction?

To be eligible to claim the super contribution as a tax deduction, you need to submit a valid ‘Notice of Intent’ form to your super fund within required time frames. You will also need to receive an acknowledgement from the super fund before you complete your tax return, start a pension, withdraw or rollover money from the fund or scheme to which you made your personal contribution.

Make sure you can utilise the deduction

It is generally not tax-effective to claim a tax deduction for an amount that reduces your assessable income below your tax free threshold. This is because you would end up paying more tax on the super contribution than you would save from claiming the deduction.

Other key considerations

- Personal deductible contributions count towards your ‘concessional contribution’ cap. This cap is $30,000 in FY 2024/25, or may be higher if you didn’t contribute your full concessional contribution cap in any of the previous five financial years and are eligible to make ‘catch-up’ contributions. Tax implications and penalties may apply if you exceed your cap.

- You can’t access super until you meet certain conditions.

- If you are an employee, another way you may be able to grow your super tax effectively is to make salary sacrifice contributions (see below)

Seek advice

To find out whether you could benefit from this strategy, you should speak to an independent financial adviser and a registered tax agent.

Case study

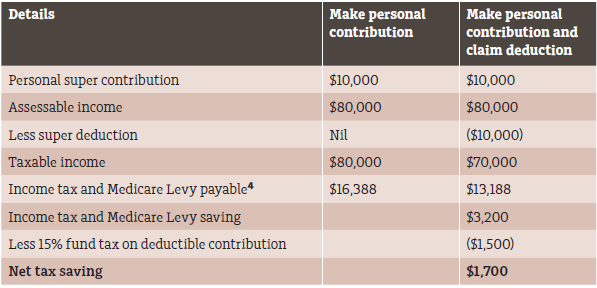

Bill, aged 55, is self-employed, earns $80,000 pa and pays tax at a marginal rate of 32% (including the Medicare levy). He plans to retire in 10 years and wants to boost his retirement savings. After speaking to an independent financial adviser, he decides to make a personal super contribution of $10,000 and claim the amount as a tax deduction. By using this strategy, he’ll increase his super balance. Also, by claiming the contribution as a tax deduction, the net tax saving will be $1,700. If the tax deduction is claimed on the personal contribution, $8,500 (his contribution net of tax withheld) is invested in super. If no deduction is claimed, $10,000 is invested in super. However, no tax savings are applied to Bill’s income tax assessment for the relevant year.

Salary sacrifice contributions

If you are an employee, you may want to arrange with your employer to contribute some of your pre-tax salary into super. This is known as ‘salary sacrifice’.

Like making personal deductible contributions, salary sacrifice may enable you to boost your super tax-effectively. There are, however, a range of issues you should consider before deciding to use this strategy.

We can help you determine whether you should consider salary sacrifice instead of (or in addition to) making personal deductible contributions.

- Individuals with income above $250,000 in FY 2024/25 will pay an additional 15% tax on personal deductible and other concessional super contributions. ↩︎

- Includes Medicare Levy. ↩︎

- Based on FY 2024/25 tax rates. ↩︎

IMPORTANT INFORMATION: This information has been prepared by Periapt Advisory Pty Ltd, ABN 67 648 208 253 AFSL 542418, based on our understanding of the relevant legislation at the time of writing. The information is of a general nature only and has been prepared without consideration of any particular individual’s objectives, financial situation, or needs. Before making any decisions, we recommend you consider independent financial advice. Current at 6 March 2025.